Atlanta Housing Affordability by Neighborhood: Income Needed in 2026

How Much Income You Need to Buy a Home in Atlanta Metro Neighborhoods (2026)

Atlanta has quietly shifted from a “value market” to a city where affordability depends heavily on exact location. In 2026, the gap between neighborhoods is no longer small, it’s the difference between a $70K salary working just fine or falling completely short.

This breakdown looks beyond averages and focuses on what buyers actually face on the ground: how much income you realistically need depending on where you buy in the Atlanta metro area.

Atlanta Housing in 2026: Still Affordable — But Narrowly

On paper, Atlanta is still cheaper than coastal markets. In practice, affordability is getting tighter every year.

- Median home price: ~$380K–$400K

- Typical monthly payment: ~$2,300–$2,800

- Estimated income needed: ~$90K–$105K

That puts Atlanta in a transitional category — not cheap, not unaffordable, but increasingly sensitive to interest rates and location choices.

For a broader comparison, see how this trend plays out nationally in our analysis:

How Much You Need to Earn to Live Alone in U.S. Cities (2026).

Income Needed by Neighborhood Tier

Atlanta isn’t a single housing market. It behaves more like a collection of smaller markets, each with its own price floor.

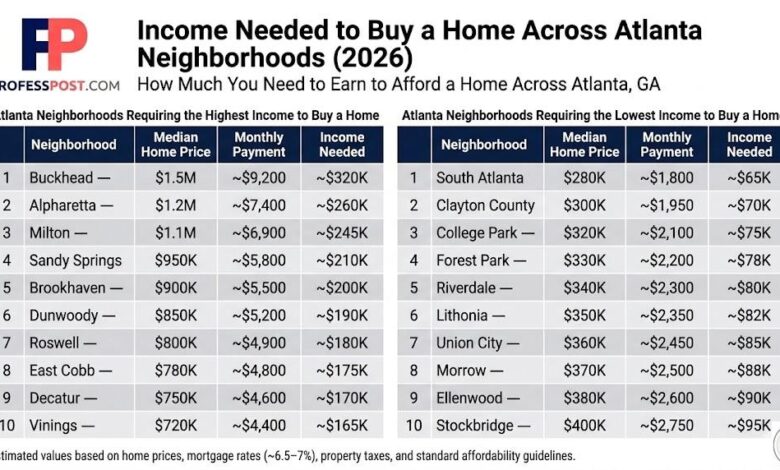

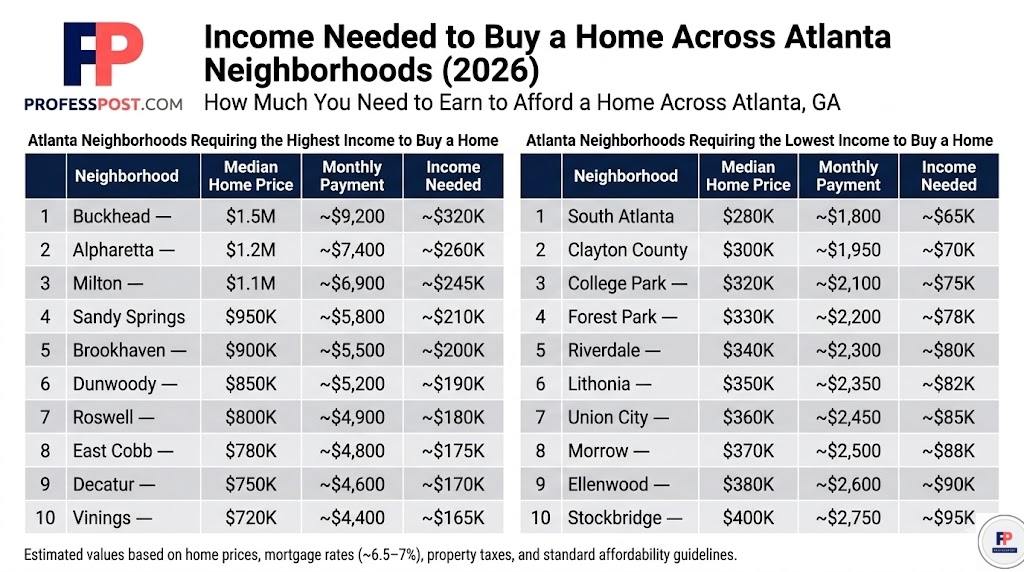

Entry-Level Areas (~$275K – $325K)

- Estimated income: $65K – $85K

- Common locations: South Atlanta, Clayton County, parts of DeKalb County

These neighborhoods remain the primary entry point for first-time buyers. However, lower prices often come with trade-offs — longer commutes, older housing stock, or fewer amenities.

Even at this level, buyers are increasingly stretching budgets, especially with current mortgage rates.

Mid-Tier Suburbs (~$375K – $500K)

- Estimated income: $95K – $130K

- Common locations: Marietta, Lawrenceville, Decatur

This is where most demand is concentrated. Dual-income households dominate this segment, and competition tends to be strongest here.

Buyers in this range are often balancing affordability with commute times and school quality.

Upper-Tier Neighborhoods (~$600K – $900K)

- Estimated income: $140K – $220K

- Common locations: Sandy Springs, Brookhaven, Roswell

At this level, affordability becomes much more sensitive to interest rates. Even small changes in financing costs can shift required income by tens of thousands.

High-End & Luxury Areas ($1M+)

- Estimated income: $250K – $400K+

- Common locations: Buckhead, Alpharetta, Milton

These markets are less constrained by affordability and more driven by income concentration and lifestyle preferences.

Compared to coastal luxury markets, Atlanta still offers more space for the price — but the income barrier is firmly in top-earner territory.

Why Location Matters More Than Income in Atlanta

One of the defining characteristics of Atlanta’s housing market is how dramatically prices shift over short distances.

Crossing from Inside the Perimeter (ITP) to Outside the Perimeter (OTP) can significantly change:

- Home prices

- Property taxes

- Commute times

- Overall affordability

This creates a situation where two households earning the same income can have completely different homeownership outcomes — simply based on where they choose to buy.

We explored a similar affordability gap in high-cost markets here:

What a $200K Salary Really Buys in Major U.S. Cities.

The Real Constraint: The Margin of Affordability

The key issue in Atlanta isn’t whether buyers can qualify for a mortgage — it’s how little financial room they have left after doing so.

For many households:

- Housing costs consume ~28%–32% of income

- Rising insurance and taxes add pressure

- Interest rate changes have an outsized impact

This means affordability exists — but often without much flexibility.

In practical terms, buyers are increasingly making trade-offs between:

- Location vs. price

- Home size vs. commute

- Monthly payment vs. long-term financial stability

Bottom Line

Atlanta is no longer a “low-cost alternative” — it’s a market where affordability depends on precision.

Buyers who approach the market with flexibility — especially around location — have far more options.

Those targeting specific high-demand neighborhoods will need significantly higher incomes to compete.

The takeaway is simple: in Atlanta, where you buy matters just as much as how much you earn.

Methodology

This analysis estimates the income required to purchase homes across different Atlanta metro neighborhoods using a standardized affordability model.

Key assumptions include:

- Mortgage rate: 6.5% – 7.0% (30-year fixed)

- Down payment: 10% – 20%

- Property tax rate: ~0.9% – 1.2% annually (varies by county)

- Homeowners insurance: Estimated based on Georgia averages

- Debt-to-income (DTI) ratio: 28% front-end guideline

Monthly housing costs include principal, interest, property taxes, and insurance (PITI).

Income estimates are calculated based on keeping housing costs within standard affordability thresholds used by lenders.

Neighborhood price tiers are based on recent listing data, median home values, and regional housing trends rather than individual listings.

Sources

- Zillow Home Value Index (ZHVI)

- Redfin Housing Market Data

- U.S. Census Bureau (income benchmarks)

- Federal Reserve Economic Data (FRED)

- Local Georgia property tax estimates

- Mortgage rate averages (Freddie Mac PMMS)

All figures are estimates intended to reflect typical market conditions in 2026. Actual affordability will vary based on credit profile, loan structure, and timing.