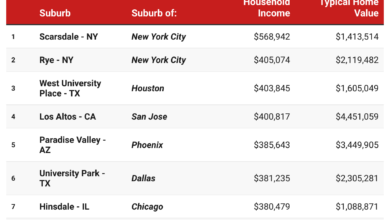

What a $200K Salary Really Buys in 5 Major U.S. Cities (2026 Housing Reality)

What does a $200K salary really buy in today’s housing market?

Not long ago, earning $200,000 a year meant you could afford a comfortable home in almost any U.S. city. In 2026, that assumption no longer holds.

The modern housing market has become deeply fragmented — not just between states, but between individual cities and even neighborhoods. The same income now delivers completely different outcomes depending on where you try to buy.

This analysis looks at five major U.S. cities — New York City, San Francisco, San Die, go, Austin, and Chicago — to understand what $200K actually buys today, and how local housing dynamics shape affordability.

🇺🇸 The National Context: A Higher Barrier to Entry

Across the U.S., housing affordability has shifted dramatically in recent years.

- The average U.S. home value is now around $350K–$400K+

- The income required to afford a median-priced home is roughly $106K+

- The median U.S. household income remains significantly lower (~$80K range)

This gap explains why homeownership is becoming increasingly difficult — especially in major metro areas where prices are far above the national average.

In high-cost cities, affordability isn’t just stretched — it’s structurally out of reach for many households.

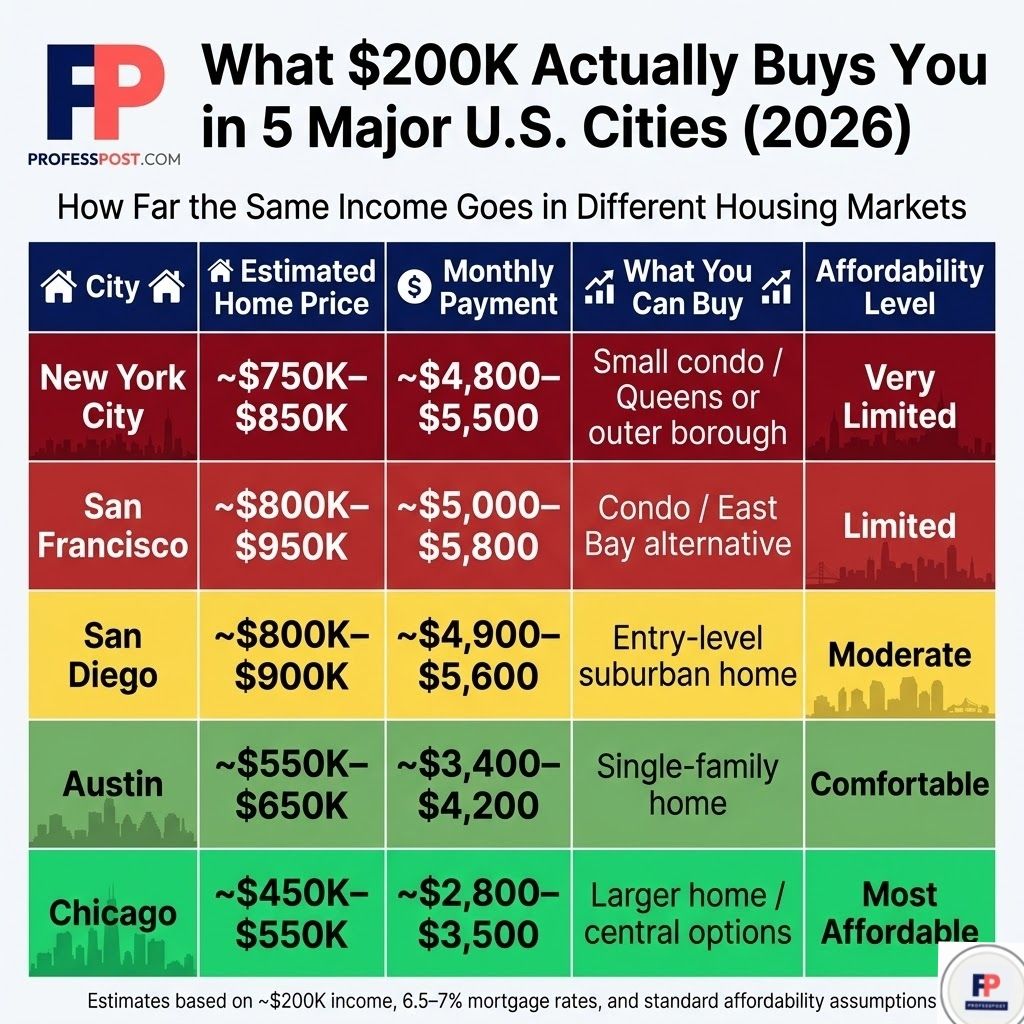

New York City: High Prices, Limited Entry Points

New York remains one of the most complex housing markets in the country.

The median home price across NYC is roughly $750K–$800K, with Manhattan often exceeding $1.2M

At a $200K income:

- Buyers are largely priced out of Manhattan ownership

- Most realistic options are co-ops or condos in Queens or parts of Brooklyn

- Strict co-op rules and high monthly fees further limit access

NYC is less about what you can afford — and more about what compromises you’re willing to make.

👉 See detailed rent pressure by neighborhood:

NYC Rent-to-Income Breakdown

San Francisco: High Income, High Constraints

San Francisco continues to be defined by limited supply and high-income demand.

Even as prices fluctuate, competition remains intense due to tech-driven demand and low inventory levels

At $200K income:

- Buyers typically afford smaller condos rather than single-family homes

- HOA fees — often exceeding $500/month — add significant cost

- Many buyers look to the East Bay for better value

Affordability here isn’t just about price — it’s about ongoing ownership costs.

👉 Neighborhood-level breakdown:

San Francisco Affordability by Neighborhood

San Diego: The Lifestyle Premium

San Diego combines strong demand with limited supply, creating one of the tightest housing markets in the country.

Median home prices have approached $850K–$900K in recent years.

At $200K income:

- Buyers can access entry-level homes in suburban areas

- Coastal neighborhoods remain largely unaffordable

- The price gap between “starter” and “prime” locations is unusually wide

This creates a clear trade-off: location vs affordability.

👉 Full neighborhood comparison:

San Diego by Neighborhood

Austin: More Space, But Changing Fast

Austin has long been seen as a more affordable alternative — but that gap has narrowed.

Even with recent rent declines, home prices remain elevated due to population growth and sustained demand.

At $200K income:

- Buyers can still afford single-family homes

- More neighborhood flexibility compared to coastal cities

- However, affordability has declined significantly since 2020

Austin represents the “middle ground” — still accessible, but no longer cheap.

👉 See detailed breakdown:

Austin Neighborhood Analysis

Chicago: One of the Last Affordable Major Cities

Chicago stands out among major U.S. cities for its relative affordability.

While prices have increased, they remain far closer to the national average compared to coastal markets.

At $200K income:

- Buyers can afford larger homes or central locations

- Less pressure to compromise on space or neighborhood

- More balanced price-to-income ratio

This makes Chicago one of the few large cities where homeownership remains broadly attainable for upper-middle-income households.

The Real Difference: Same Income, Different Outcomes

Looking across these five cities, the contrast is clear:

- In NYC and San Francisco, $200K often means compromise

- In San Diego, it means trade-offs

- In Austin, it provides flexibility

- In Chicago, it still delivers comfort

The key takeaway is simple:

Housing affordability in the U.S. is no longer about income alone — it’s about geography.

Methodology

This analysis is based on a standardized affordability model:

- Household income: $200,000

- Down payment: 20%

- Mortgage rate: ~6.5%–7%

- Affordability rule: Housing costs ≤ 30% of gross income

Estimated home price ranges reflect what buyers can afford under these assumptions, including:

- Principal and interest

- Property taxes

- Home insurance

- Typical HOA fees (where applicable)

City-specific insights are adjusted based on local market conditions such as inventory constraints, demand patterns, and housing types.

👉 Related cost pressure:

Home Insurance Costs by City

Sources

- Zillow Home Value Index (U.S. and city-level trends)

- Redfin Housing Market Data

- National Association of Realtors (NAR)

- Visual Capitalist affordability analysis

- PropertyShark NYC market data

- Yahoo Finance & Redfin national housing data

- Recent housing market news (San Francisco, San Diego trends)

Final Thought

A $200K salary hasn’t changed — but what it buys has.

In today’s market, choosing where to live is no longer just a lifestyle decision.

It’s a financial strategy.