How Much Income You Need to Buy a Home in Austin by Neighborhood

Income Needed to Buy a Home in Austin by Neighborhood (2026)

Austin’s housing market has gone through a major shift over the past few years. While home prices have cooled slightly since their peak, affordability remains a major challenge—especially in central neighborhoods.

As of 2026, the median home price in Austin is still around $520,000 to $540,000, with average home values near $500,000. This means that even “average” homes now require a six-figure income to afford comfortably.

But the real story is how much this number changes depending on where you buy. In some Austin neighborhoods, you need over $500,000 per year to afford a home, while in others, the required income is closer to $100,000.

For broader context on how housing costs impact affordability across the country, see our analysis of

home insurance costs across major U.S. cities and how they affect total ownership expenses.

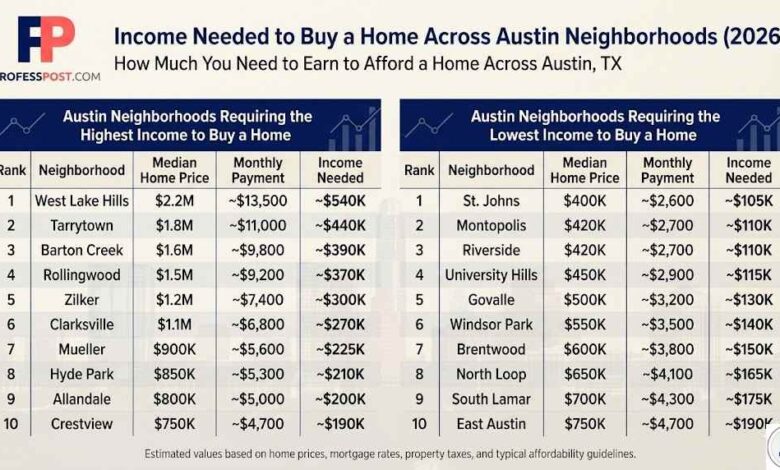

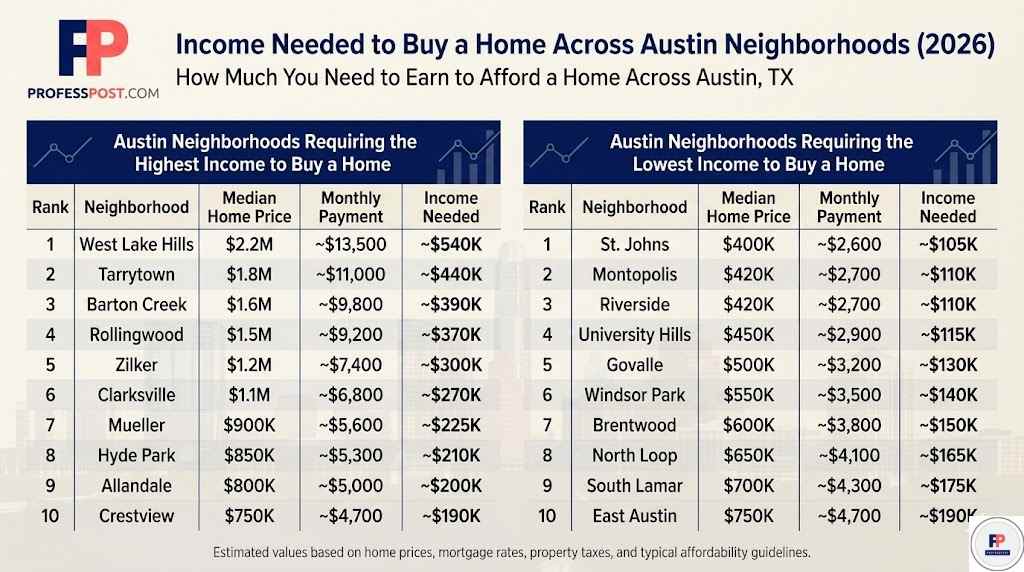

Austin Neighborhoods Requiring the Highest Income to Buy a Home

| Rank | Neighborhood | Median Home Price | Monthly Payment | Income Needed |

|---|---|---|---|---|

| 1 | West Lake Hills | $2.2M | ~$13,500 | ~$540K |

| 2 | Tarrytown | $1.8M | ~$11,000 | ~$440K |

| 3 | Barton Creek | $1.6M | ~$9,800 | ~$390K |

| 4 | Rollingwood | $1.5M | ~$9,200 | ~$370K |

| 5 | Zilker | $1.2M | ~$7,400 | ~$300K |

| 6 | Clarksville | $1.1M | ~$6,800 | ~$270K |

| 7 | Mueller | $900K | ~$5,600 | ~$225K |

| 8 | Hyde Park | $850K | ~$5,300 | ~$210K |

| 9 | Allandale | $800K | ~$5,000 | ~$200K |

| 10 | Crestview | $750K | ~$4,700 | ~$190K |

In Austin’s most expensive neighborhoods, homeownership has increasingly become a high-income benchmark. Areas like West Lake Hills and Tarrytown combine limited housing supply with strong demand, pushing both home values and required incomes far above national averages.

Austin Neighborhoods Requiring the Lowest Income to Buy a Home

| Rank | Neighborhood | Median Home Price | Monthly Payment | Income Needed |

|---|---|---|---|---|

| 1 | University Hills | $450K | ~$2,900 | ~$115K |

| 2 | Montopolis | $420K | ~$2,700 | ~$110K |

| 3 | St. Johns | $400K | ~$2,600 | ~$105K |

| 4 | Riverside | $420K | ~$2,700 | ~$110K |

| 5 | Govalle | $500K | ~$3,200 | ~$130K |

| 6 | Windsor Park | $550K | ~$3,500 | ~$140K |

| 7 | Brentwood | $600K | ~$3,800 | ~$150K |

| 8 | North Loop | $650K | ~$4,100 | ~$165K |

| 9 | South Lamar | $700K | ~$4,300 | ~$175K |

| 10 | East Austin | $750K | ~$4,700 | ~$190K |

Even in Austin’s more “affordable” neighborhoods, the income required to buy a home is still well above the national median. This reflects a broader trend where rising home prices continue to outpace income growth.

For a deeper breakdown of how income translates into real affordability, see our analysis of

how salaries feel across U.S. cities.

Why Income Requirements Vary So Much

The gap between neighborhoods is largely driven by home values. In Austin, housing remains the biggest factor in determining affordability, with property taxes alone often reaching around 2% of a home’s value annually.

Additionally, local market conditions have shifted. While prices have stabilized or slightly declined in recent years, affordability remains tight due to high mortgage rates and elevated baseline prices.

For a broader look at housing trends, see our analysis of

home price changes across U.S. counties.

Methodology

This analysis estimates the income required to afford a home using a standardized framework:

- 20% down payment

- 30-year fixed mortgage

- Mortgage rates between 6.5% and 7%

- Property taxes and insurance included

- Monthly housing costs capped at ~33% of gross income

Home price estimates are based on recent market data and neighborhood-level trends. The income figures represent the estimated salary needed to comfortably afford monthly housing costs under typical lending guidelines.

Sources

- U.S. Census Bureau – Median Household Income Data

- Zillow Research – Home Value Index and Market Trends

- Federal Reserve Economic Data (FRED) – Mortgage Rates

- Consumer Financial Protection Bureau (CFPB) – Mortgage Affordability Guidelines

- National Association of Realtors (NAR) – Housing Affordability Metrics

- Texas Comptroller – Property Tax Data and Estimates

Related Analysis

The Bottom Line

In Austin, the income needed to buy a home can vary by more than $400,000 depending on the neighborhood. While some areas remain relatively accessible, many central neighborhoods now require incomes well above $200,000.

This highlights a growing divide between income growth and housing affordability—not just in Austin, but across many major U.S. cities.

About the Author

This article was written by the ProfessPost research team, focusing on U.S. housing markets, income trends, and real estate affordability. Our goal is to break down complex financial data into clear, actionable insights for readers.